What Benefits Are Married Couples Entitled To? Understanding Your Rights and Advantages

Married couples have access to several important benefits that can enhance their financial security and well-being. You may be eligible for various Social Security benefits, tax breaks, and retirement account advantages simply because you are married. Understanding these benefits is key to making informed financial decisions together.

For instance, Social Security allows one spouse to claim benefits based on the other spouse’s work history, which can be particularly beneficial if one partner earned significantly more than the other. Additionally, couples can take advantage of tax benefits that may lower their overall tax burden, such as filing jointly.

It’s essential to stay informed about the benefits available to you as a married couple. Knowing your options can help maximize your financial resources and support your family’s future.

Understanding Social Security Benefits

Social Security benefits play a critical role in ensuring financial support for married couples. Knowing what these benefits entail and how full retirement age affects them can help you make informed decisions about your future.

What Social Security Entails

Social Security is a government program that provides financial support to retirees, disabled individuals, and their families. For you, as a married couple, it includes potential benefits based on your work records as well as your spouse’s. Each of you pays into the system through Social Security taxes deducted from your paychecks.

To qualify for benefits, you need enough work credits, usually obtained by working for at least 10 years. If you don’t have enough credits, you may still receive spousal benefits based on your spouse’s earnings. This ensures you can access financial help even if your own work history is limited.

The Impact of Full Retirement Age on Benefits

Your full retirement age (FRA) is the age when you can receive 100% of your Social Security benefits. It varies based on your birth year. If you claim benefits before your FRA, your monthly benefit amount may be reduced.

For example, if you and your spouse wait until your FRA to claim benefits, you can maximize the amount you receive. If your spouse’s earnings were higher, you might consider claiming benefits based on their record. This could be up to half of their primary insurance amount if it’s greater than your own benefit.

Make sure to check with the Social Security Administration for details relevant to your specific situation. Planning ahead can help you make the most of the benefits available to you.

Eligibility and Filing for Married Couples

When you are married, you and your spouse may have access to various financial benefits through Social Security. It’s important to understand how eligibility works and the steps required to claim these benefits.

Determining Eligibility for Spousal Benefits

To qualify for spousal benefits, you must meet specific eligibility criteria. You need to be married to someone who qualifies for Social Security benefits. If you are divorced, you can still claim benefits based on your former spouse’s work record if you were married for at least 10 years.

Key eligibility conditions include:

- Both spouses must be at least 62 years old.

- You must be currently married or divorced, not separated.

- Same-sex couples in valid marriages also can claim spousal benefits.

Make sure to check if you are eligible for deemed filing, which means you have to apply for both your benefits and your spouse’s simultaneously.

Procedures for Claiming Spousal Benefits

Claiming spousal benefits involves a few important steps. First, you should gather your spouse’s work history details and your own Social Security number. Then, determine the best time to file based on your ages and financial needs.

You can apply online, by phone, or at your local Social Security office. Here’s what you need:

- Your marriage certificate.

- Your spouse’s Social Security number.

- Identification and proof of age.

Remember, if you delay filing your own benefits, you might get a higher payment later on. Each couple can have different strategies, so it’s good to explore all options with your spouse.

Maximizing Retirement Benefits

When planning for retirement, knowing how to manage your benefits can make a big difference. Using strategies effectively can help you and your spouse maximize your retirement income. Here’s how you can benefit from delayed retirement credits and strategic claiming.

Leveraging Delayed Retirement Credits

When you delay claiming Social Security past your full retirement age, you gain delayed retirement credits. This increase can boost your primary insurance amount each year until age 70.

For every year you wait, you could earn up to an 8% increase in benefits. If your monthly benefit at full retirement age is $2,000, waiting until 70 could raise it to about $2,640 a month.

These credits can significantly increase your total retirement income. Plus, if both you and your spouse use this strategy, your combined benefits could be much higher.

Strategies for Claiming Benefits

Creating a smart claiming strategy is key to maximizing benefits. For married couples, it’s essential to understand spousal benefits. You can claim your Social Security based on your spouse’s earnings record if it’s higher than your own.

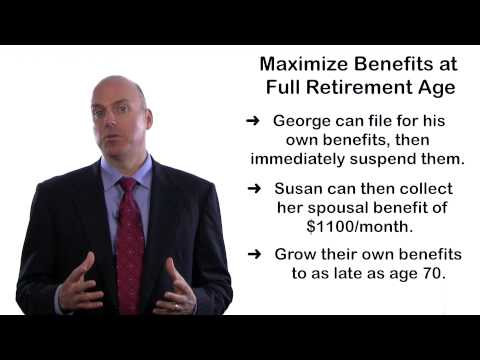

You can also consider the file and suspend option. This allows one spouse to claim a benefit while the other delays, letting the latter accrue more benefits.

Knowing the maximum spousal benefit can help you decide the best time to claim. The spousal benefit can be up to 50% of your partner’s benefit at full retirement age.

Thinking carefully about your working years, retirement savings, and claiming age will help you strengthen your financial future together.

Considerations for Special Situations

When it comes to Social Security benefits, certain situations might change your eligibility or the amount you can receive. Special cases like survivor benefits and benefits for divorced spouses are important to understand. Let’s take a closer look.

Understanding Survivor Benefits

Survivor benefits are designed to help the family of a deceased worker. If your spouse passes away, you might be eligible for their survivor benefits. This payment can be higher than your own Social Security benefit.

To qualify, you must be at least 60 years old or 50 years old if you are disabled. The benefit amount is based on the deceased spouse’s Primary Insurance Amount (PIA). This means you can receive a percentage of what they would have gotten if they were still alive.

Make sure to apply for these benefits soon after your spouse’s death. The application process can be done through the Social Security Administration, either online or in person. It’s a good idea to gather necessary documents, like your marriage certificate and your spouse’s death certificate.

Benefits for Divorced Spouses

If you and your ex-spouse were married for at least 10 years, you may qualify for Social Security benefits based on their work record. This is a critical point if you have a limited earnings history.

You can claim either your own benefit or up to 50% of your ex-spouse’s PIA, whichever is higher. To receive these benefits, you must be unmarried and at least 62 years old.

If your ex-spouse is deceased, you could receive survivor benefits instead if you qualify. It’s also important to know that your benefit won’t affect your ex-spouse’s benefits. Make sure to contact the Social Security office to get all the details you need for your specific situation.